Smith+Nephew: A Deep Dive into a MedTech Giant

The Hull Chemist That Helps 14 Million People Walk, Move, and Heal

The Story of Elastoplast: A Name That Heals

Whenever someone in my family gets a cut or scrape—whether it’s my child falling on the playground or an elderly with thin, delicate skin—I instinctively reach for one thing: Elastoplast.

That little red-and-white box has been in our drawers for years. We call it a bandage, but truthfully, we often just say "put some Elastoplast on it." That’s the power of a brand—it becomes a part of daily life, a part of our care.

But where did Elastoplast come from?

Let me take you back to 1920. Smith & Nephew, a company that started in a small pharmacy in Hull, England, introduced Elastoplast as one of the first adhesive wound dressings. It was simple but revolutionary. People no longer needed to wrap large cloth bandages for small wounds—now they had a ready-to-use strip that stuck to the skin and protected the cut.

Elastoplast became more than a product. It became a symbol of care—for mums patching up scraped knees, for nurses tending to patients, for athletes with bruised elbows. From households to hospitals, its name spread far and wide. By the mid-20th century, Elastoplast was a household name across the UK, Europe, and even Australia.

Image: Elastoplast develoved by Smith & Nephew, The brand was sold in 2001 to Beiersdorf

Though many don’t realise it, Smith & Nephew no longer owns Elastoplast. In 2001, the brand was sold to Beiersdorf, a German company also known for Nivea. Smith & Nephew had started to focus more on high-tech wound care and surgical innovations—big things like robotics and joint replacements. But the name Elastoplast stayed close to our hearts.

Even today, when I open that little box, I feel a sense of comfort. It reminds me that some things—like caring for those we love—never go out of style.

I have done a deep dive analysis on Smith & Nephew as part of my Finota series. In this report, I explore how a company that once brought us the household name Elastoplast—a staple in family first-aid kits—has transformed into a global leader in medical technology.

This analysis covers:

Revenue drivers across their three core business units—Orthopaedics, Sports Medicine & ENT, and Advanced Wound Management

The impact of innovation—with over 60% of 2024’s growth coming from products launched in just the last five years

The execution of the 12-Point Plan that’s helping fix legacy issues and lift margins

Smith & Nephew’s role in treating 14 million patients a year, and the global demand shaping its market

What all of this means for long-term investors—opportunities, risks, and room for re-rating

Smith & Nephew’s story is not just about products. It’s about how we care, heal, and invest in the future of health. Let’s dive in.

Introduction and History of Smith+Nephew

Smith+Nephew is a 168-year-old medical technology company with humble origins and a rich history. It began in 1856 when Thomas James Smith opened a small pharmacy in Hull, England, developing improved methods for refining cod liver oil . In 1896, his nephew Horatio joined, and the business became T.J. Smith & Nephew, laying the foundation for a family enterprise that would expand into wound care and surgical supplies . The company’s big break came during World War I, when it secured urgent contracts to supply field dressings, rapidly growing its staff from 50 to 1,200 to meet wartime demand .

Throughout the 20th century, Smith+Nephew introduced iconic products and milestones. In 1928 it launched Elastoplast, an innovative adhesive bandage that became a household name . The company went public on the London Stock Exchange in 1937 , marking its emergence as an established healthcare firm. Post-war, Smith+Nephew continued innovating – for example, developing special plaster casts for the 1953 Everest expedition, and later expanding into surgical instruments and dressings as medicine advanced .

From the 1980s onward, Smith+Nephew transformed into a global medical technology (medtech) leader through strategic acquisitions and product innovation. Key acquisitions included Richards Medical (orthopaedic implants) and Dyonics (arthroscopy instruments) in 1986, expanding the company into Orthopaedics and Sports Medicine devices . In the 1990s, Smith+Nephew entered the U.S. market in force – acquiring companies like Acufex (1995) to lead in minimally invasive arthroscopic surgery . It dual-listed on the New York Stock Exchange in 1999 and joined the FTSE-100 index by 2001 . The 2000s saw further breakthroughs, such as the introduction of OXINIUM◊ oxidized zirconium alloy for joint implants in 2001, extending implant longevity , and PICO◊ in 2011, a pocket-sized negative-pressure wound therapy device that revolutionized wound care .

Today, Smith+Nephew is truly global – operating in over 100 countries with ~17,000 employees – yet it remains anchored by its founding mission of healing. Headquartered in London, it has become a portfolio medtech business spanning orthopaedic reconstruction, sports injuries, ear-nose-throat (ENT) treatments, and advanced wound management. Despite being a century-and-a-half old, the company continues to innovate and grow. It generated $5.8 billion in annual sales in 2024 and has paid dividends every year since 1937, reflecting a legacy of stability for investors . From a small Hull pharmacy to a multinational FTSE-100 company, Smith+Nephew’s journey exemplifies enduring innovation in service of patients.

Purpose and Mission: “Life Unlimited”

Smith+Nephew’s corporate purpose is encapsulated in two words: Life Unlimited. This phrase defines the company’s mission to restore not just bodies but also self-belief, enabling people to live without the limitations of pain or disability. As the company explains, physical health is intertwined with mental wellbeing and aspirations – when an injury or condition holds someone back, “it’s our whole life on hold”. Smith+Nephew exists to change that story. It leverages technology and medical innovation to “take the limits off living”, helping patients regain mobility, confidence, and quality of lifefile.

This patient-centric purpose comes to life in many inspiring stories. For example, a farmer with a severe knee injury can get back to work and provide for his family after a Smith+Nephew knee implant; a grandparent with a new hip can play with grandchildren again; an athlete with a repaired shoulder tendon can return to the sport they love. Such narratives drive home the real-world impact of the company’s devices. Smith+Nephew often highlights real patient case studies – people staring down fear, overcoming pain, and proving “anything is possible” once healed. These stories illustrate Life Unlimited in action: technology enabling patients to go on stronger than before.

Importantly, Life Unlimited also shapes the company’s culture and values. Smith+Nephew fosters a culture of Care, Courage, and Collaboration – caring for patients and each other, having courage to innovate, and collaborating to solve healthcare challenges. Every employee is encouraged to connect their daily work to the ultimate purpose of improving patients’ lives. This shared sense of mission not only inspires innovation but also underpins Smith+Nephew’s commitment to operating responsibly and ethically. In short, Life Unlimited is more than a slogan – it’s the guiding star for how Smith+Nephew designs products, serves medical professionals, and makes decisions to positively impact society.

Industry Update

Smith & Nephew operates in the global medical technology industry, primarily across orthopaedic reconstruction, sports medicine & ENT, and advanced wound management segments. These markets are sizable and growing steadily. For example, the hip and knee implant market is about $16.8 billion in 2024, growing ~5% annually. The trauma & extremities segment adds another $14.6 billion, rising ~7%, reflecting increasing injury treatments and an aging population. In sports medicine (excluding ENT), Smith & Nephew competes in a $6.1 billion market growing ~5%, while advanced wound care is around $12.5 billion (+6%) globally. These growth rates outpace general GDP, driven by favorable demographics and healthcare trends. An aging and more active population is fueling demand – as people live longer and pursue active lifestyles, the prevalence of degenerative joint conditions, sports injuries, diabetes and chronic wounds has risen. This creates tailwinds for joint replacements, ligament repairs, and wound therapies.

Key industry segments align with Smith & Nephew’s portfolio: reconstructive implants (hips, knees, shoulders), trauma fixation devices (plates, screws, nails), sports medicine biologics and instruments (for arthroscopy and soft-tissue repair), ENT surgical tools, and advanced wound dressings and devices. Each segment has distinct economic and regulatory factors. Reimbursement environments and cost pressures are notable – hospitals and payers worldwide seek value for money, sometimes via bundled payments or competitive tenders. In China, for instance, the government’s Volume-Based Procurement (VBP) program has imposed unilateral price cuts on orthopaedic implants, creating a significant headwind in that market. Regulatory approval pathways (e.g. FDA in the US, CE marking in Europe) require rigorous clinical evidence and quality manufacturing, raising barriers but ensuring patient safety.

Technology plays a transformative role across the industry. There is a clear trend toward robotic-assisted surgery and digital enabling technologies to improve precision and outcomes. Smith & Nephew has capitalized on this, noting that its CORI surgical robot was the first in the industry cleared for revision knee procedures. Surgeons are increasingly adopting robotics – roughly one-third of knee replacements in the US are now performed with robotic assistance – and companies with robotic platforms and navigation software (like Smith & Nephew’s CORI and RI.HIP navigation) are positioned to benefit. Another major trend is the shift of procedures from hospitals to outpatient ambulatory surgery centers (ASCs) for cost efficiency and patient convenience. Smith & Nephew explicitly notes this shift in both orthopaedics and sports medicine and has tailored offerings for the ASC setting. Additionally, biologics and regenerative technologies are gaining ground – for example, bioengineered implants that help tissues heal (an area where Smith & Nephew’s REGENETEN implant is pioneering an 86% reduction in rotator-cuff re-tear rates). In wound care, negative pressure wound therapy (NPWT) devices and advanced dressings illustrate how innovation can accelerate healing while reducing complications and hospital stays. Overall, technology is enabling better outcomes with less invasive procedures and faster recoveries, a value proposition welcomed by patients and payers alike.

Competitive Landscape

The medical device industry is highly competitive, with a few dominant players in each segment. Smith & Nephew, despite its UK base, competes mostly with large US-based multinationals. In orthopaedic reconstruction (hips and knees), it is one of four leaders alongside Stryker, Zimmer Biomet, and DePuy Synthes (J&J). These giants command the bulk of global market share – for instance, Zimmer and Stryker together hold over 50%, whereas Smith & Nephew has about a 10% share in hip and knee implants. This indicates significant room for Smith & Nephew to grow if it can capture share from competitors. In Sports Medicine, Smith & Nephew is a top-tier player – it holds roughly 28% of the global sports medicine market, second only to private competitor Arthrex (33% share) and ahead of Stryker (12%) and J&J’s DePuy Mitek (10%). In Advanced Wound Management, Smith & Nephew is the #2 player worldwide (14% share), closely following the segment leader (recently spun-off as “Solventum”, formerly part of 3M, at ~15% share). Other wound care competitors include Mölnlycke (Sweden) and ConvaTec (UK) in advanced dressings. This diversified competitive field means Smith & Nephew faces pressure on multiple fronts: from orthopaedics powerhouses to niche specialists.

Competitive pressures are intense. Rival firms invest heavily in R&D and salesforce to win hospital contracts and surgeon loyalty. Pricing pressure is a constant, not only from government initiatives like VBP but also from hospital group purchasing organizations (GPOs) and insurers in the US that negotiate discounts. The industry also sees periodic waves of consolidation: big players acquire smaller innovators to broaden their portfolio (for example, Stryker’s acquisition of Mako Surgical to obtain a robotic system). This raises entry barriers – new entrants must bring truly disruptive technology to break in, given the incumbents’ scale in manufacturing, distribution, and regulatory expertise. Barriers to entry are indeed high: products require regulatory approval, extensive clinical validation, and specialized sales channels where relationships with surgeons are crucial. Smith & Nephew’s own 160+ year legacy and global sales network illustrate how hard it is for a newcomer to replicate such footprint.

However, emerging competitors are on the horizon in certain niches. In sports medicine, for instance, privately-held Arthrex has been highly disruptive with aggressive innovation and surgeon education programs. In wound care, smaller biotech firms are developing novel skin substitutes and growth factor therapies that could compete with traditional wound dressings. Moreover, in price-sensitive markets like China, local device manufacturers are beginning to gain traction (often supported by policies like VBP that favor cost-effective local products). Smith & Nephew acknowledges these trends and is responding by differentiating through innovation and value. Its unique materials (like OXINIUM alloy for implants) and proprietary products aim to set it apart from mere commodity offerings.

competition is characterized by a few large rivals (with Smith & Nephew often in the top 3–4 by share), high customer bargaining power, and a need for continuous innovation. Smith & Nephew’s global market presence (it sells in over 100 countries) and broad portfolio give it resilience, but it must keep demonstrating superior clinical and economic outcomes to win contracts over formidable opponents. The fact that it maintains leadership positions – #2 in sports medicine and #2 in advanced wound care globally – shows it can hold its ownfile. Competitive rivalry will likely remain vigorous, but Smith & Nephew’s multi-segment presence also provides some balance (weakness in one area can be offset by strength in another). Continued focus on surgeon training, evidence generation, and portfolio breadth will be key to defend and grow its market positions in this landscape.

Company Overview

Smith & Nephew has a rich history and evolution. It traces its roots back over 165 years to 1856, when founder Thomas James Smith opened a small pharmacy in Hull, England. After Thomas’s death, his nephew Horatio Nelson Smith took over in 1896 – giving the company its namesake “Smith & Nephew”. Early on, the business built a reputation in wound care (supplying medical dressings, especially during World War I) and expanded steadily. By the late 20th century, Smith & Nephew had grown into a diverse healthcare company, making not just medical devices but also consumer health products. A major strategic shift came in 1998: the company restructured to focus on three high-growth franchises – Advanced Wound Management, Endoscopy (minimally invasive surgery), and Orthopaedics. This meant divesting lower-growth units and doubling down on medical technologies. In 2001, the endoscopy and orthopaedics divisions merged into an Advanced Surgical Devices division, and later in 2015 all divisions were unified, reflecting the company’s integrated global structure.

Smith & Nephew has been a publicly listed company for decades. It floated on the London Stock Exchange in 1937 and later obtained a secondary listing on the New York Stock Exchange in 1999. It’s now a constituent of the FTSE 100 index, cementing its status as one of the UK’s largest public companies. There is no majority shareholder; ownership is widely dispersed among institutional investors and pension funds. The company is truly multinational in scope – it generates over half of its revenue in the US, around one-third in Europe and other developed markets, and the remainder in emerging markets. Such broad ownership and customer base align with its identity as a global medtech leader.

Corporate leadership and culture: Smith & Nephew’s top management is relatively new, signaling a refreshed strategic direction. Dr. Deepak Nath was appointed Chief Executive Officer in April 2022, coming from a background at Siemens Healthineers and Abbott, with a mandate to accelerate growth and improve efficiency. Under his leadership, the company launched a 12-point productivity plan (more on that later) and has focused on innovation and simplification. The finance helm also changed – John Rogers joined as Chief Financial Officer in 2023, bringing experience from the consumer sector. The Board of Directors is a mix of medical industry veterans and financial experts, and governance practices meet UK corporate standards (with independent committees for audit, remuneration, etc.).

Employee sentiment appears positive. On Glassdoor, Smith & Nephew scores around 4.0 out of 5, with over 80% of employees saying they would recommend the company to a friendglassdoor.com.au. Common themes in employee reviews include pride in the mission of “Life Unlimited” (the company’s motto of restoring patients to health), and appreciation for the collaborative culture and benefits. The company emphasizes its core values of Care, Courage, and Collaboration in building a respectful workplace. Internal surveys echo this positivity – Smith & Nephew’s employee engagement (measured by Gallup) rose to around the 61st percentile globally, and voluntary turnover fell to 9.5%, a marked improvement from prior years. In fact, the company’s engagement efforts earned it Gallup’s Exceptional Workplace Award, highlighting a commitment to its people. Of course, like any large organization, there are areas to improve (some reviews cite bureaucracy or the need for clearer career paths), but overall Smith & Nephew is seen as a rewarding place to work, with employees motivated by the real-world impact of their products.

From a corporate structure and ownership perspective, Smith & Nephew is a public limited company headquartered in London. It has a decentralized operational structure divided by franchises and regions. The absence of a founder-led ownership (the founding Smith family is no longer involved) means the company is guided purely by its executive team and board on behalf of shareholders. The largest shareholders are typically institutional investors (e.g. BlackRock, Vanguard and UK-based fund managers) each holding a few percent of the stock – no single investor has a controlling stake. This broad ownership base and FTSE100 membership confer robust governance oversight and high transparency.

Management incentives are aligned with performance: top executives have significant portions of pay tied to financial results and shareholder returns. For instance, the CEO’s annual bonus can exceed 130% of base salary at maximum for hitting targets, and he also receives long-term stock awards roughly equal to 125% of salary. These performance metrics include revenue growth, trading profit margin, earnings per share, and even ESG objectives, indicating management is incentivized to deliver sustainable growth.

In summary, Smith & Nephew’s journey from a family-run wound care shop to a global surgical device powerhouse is a story of continual adaptation. It has transformed itself through strategic refocusing and acquisitions, while maintaining the original purpose of improving patient lives. The company today is professionally managed with a strong culture, enjoys a solid reputation among both employees and investors, and is positioned to leverage its heritage in modern ways. That heritage – nearly 170 years of “caring for patients” – remains a guiding light, even as the firm innovates into robotics and digital surgery.

Business Model & Products: how they make money

Smith & Nephew’s business model centers on developing and selling medical devices that repair and heal the human body, thereby enabling patients to regain their quality of life – the ethos of “Life Unlimited.” The company generates revenue primarily by manufacturing and marketing its products to hospitals, surgical centers, and clinics worldwide. Sales are carried out through a combination of a direct sales force (particularly in major markets like the US and Europe) and distributors in some regions. Its products are often “prescribed” or used by specialist physicians (orthopaedic surgeons, sports medicine surgeons, wound care nurses, etc.), which means Smith & Nephew invests heavily in clinical training and support to drive adoption.

Revenue streams and activities: The company has three major product franchises:

Orthopaedics: This includes joint replacement implants (hip and knee prostheses, and increasingly shoulder joints) and trauma hardware (plates, screws, nails for fracture fixation, plus extremity implants for hands/feet). These are typically capital goods sold per surgical procedure. Orthopaedics is the largest segment, contributing about 41% of revenue. Sales here depend on surgical volumes of joint replacements and fracture treatments, which in turn grow with aging demographics and improved access to care. Smith & Nephew also offers enabling technologies like the CORI◊ surgical robot in this segment, which can drive implant sales as an ecosystem.

Sports Medicine & ENT: This segment (around 30% of revenue covers minimally invasive surgical tools and implants for soft tissue repair – for example, devices to fix torn ligaments and tendons (in the shoulder, knee, etc.), as well as arthroscopic towers, cameras, fluid pumps, and radiofrequency probes used in keyhole surgery. The ENT portion includes devices like tonsil and adenoid removal instruments (using Smith & Nephew’s COBLATION technology). A notable aspect of this franchise is recurring revenue: many sports medicine procedures use disposable scopes, blades, or fixation implants that need restocking regularly. Thus, in addition to selling capital equipment, Smith & Nephew enjoys ongoing sales of consumables. Sports Medicine has been a high-growth, high-margin business for the company historically.

Advanced Wound Management: About 29% of revenue comes from wound care products. These range from advanced wound dressings (foams, antimicrobial gauzes like ALLEVYN and ACTICOAT) to biological therapies (skin substitutes like GRAFIX, an acquired product) and negative pressure wound therapy devices (the PICO single-use NPWT and RENASYS systems). The business model here often involves razor-and-blade dynamics: for example, selling a NPWT pump at low cost but profiting from ongoing sales of dressings/cartridges for each patient use. Wound care products improve healing in chronic wounds (like diabetic ulcers) and acute surgical incisions, helping reduce infection and complications – which makes them valuable to healthcare systems under cost pressure.

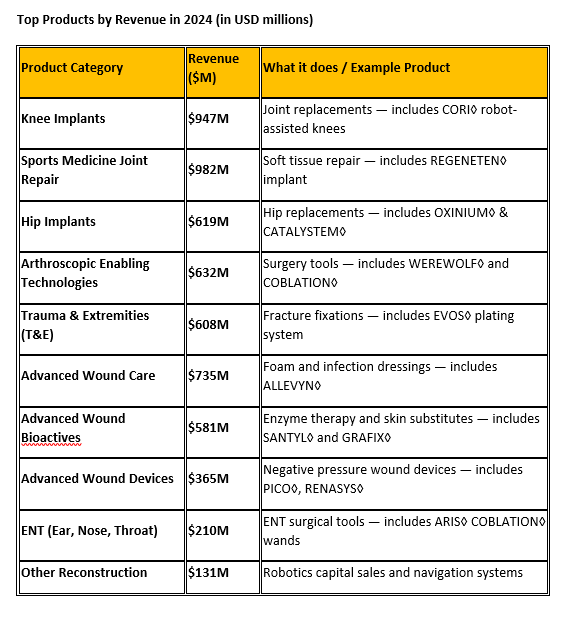

Top Products by Revenue in 2024 (in USD millions)

Smith & Nephew’s value proposition lies in offering differentiated medical solutions that improve clinical outcomes, reduce patient recovery time, and are cost-effective over the episode of care. A few key differentiators underscore this:

Innovative materials and design: The company has proprietary technology like OXINIUM, a patented oxidized zirconium alloy used in its hip and knee implants, which has superior wear characteristics – implants made with OXINIUM have lower wear and friction, potentially lasting longer than competitors’ cobalt-chrome implants. This is a clear benefit for patients (fewer revision surgeries) and a selling point to surgeons. In wound care, products like the PICO◊ single-use NPWT device allow negative pressure therapy to be delivered in a portable way, letting patients move around rather than being tethered to hospital vacuums.

Procedural innovation: Smith & Nephew doesn’t just sell devices, it often sells a procedure or technique. In sports medicine, for example, the company introduced the REGENETEN◊ bioinductive implant – a novel “patch” that is arthroscopically placed to reinforce rotator cuff tendon repairs. Clinical evidence showed REGENETEN led to an astounding 86% reduction in re-tear rates for rotator cuff surgery versus conventional repair. Such outcomes-based innovation differentiates S+N in the eyes of surgeons (who want better results for their patients). Similarly, the company’s ** JOURNEY◊ II** knee system is a kinematically-designed implant that mimics natural knee motion, aiming for more natural feeling joint function.

Holistic solutions and enabling tech: The company often bundles capital equipment with consumables to provide comprehensive solutions. A great example is the INTELLIO◊ Connected Tower for arthroscopy, which integrates visualization, fluid management, resection, and COBLATION energy devices in one system. This one-stop solution can streamline surgeries and is attractive to hospitals looking to equip operating rooms efficiently. In orthopaedics, the CORI◊ robotic system (a handheld robotic milling device) combined with Smith & Nephew’s implants allows the company to offer a cutting-edge, precise surgical solution for joint replacement. In fact, CORI’s unique design (small, portable, no pre-op CT needed) sets it apart from bulkier competitor robots, and it remains the only robotic platform indicated across partial, total, and revision knee replacements as of now.

Customer feedback and real-world impact are strong validation of Smith & Nephew’s model. Surgeons are generally loyal to technologies that demonstrably improve patient outcomes. Many of S+N’s products have become standards of care in their niches – for instance, the TRIGEN◊ INTERTAN hip fracture nail is renowned for reducing complications in hip fracture repair, and the EVOS◊ plating system is praised for its comprehensive range simplifying trauma surgeries. Patients ultimately feel the benefit: each year, roughly 14 million patients worldwide are treated with Smith & Nephew products. These include people from all walks of life – from elderly individuals walking again pain-free thanks to a new hip, to athletes getting back in the game after knee ligament repair. One compelling story highlighted by the company is that of Fireman Rob, a firefighter who, after receiving a Smith & Nephew knee implant, went on to set a world record for climbing the most stairs in full gear. Such stories exemplify the “Life Unlimited” promise in action – the products truly improve lives, restoring mobility and hope. This positive patient impact in turn builds the brand’s reputation among surgeons and healthcare providers, creating a virtuous cycle for the business.

Smith & Nephew’s business model is about selling high-quality medical devices and solutions, often with a supporting ecosystem of instruments and services, to solve unmet clinical needs. Revenue is driven by surgical volumes and the adoption of its technologies, so the company focuses on R&D, clinical evidence, and physician education to drive preference for its products. Its differentiators like advanced materials, digital surgery tools, and unique biologics give it pricing power and protect against commoditization. By continually innovating (over 50 new product launches in the last 5 years) and listening to surgeon feedback, Smith & Nephew aims to sustain its competitive edge and fulfill its mission of helping patients live their lives without limitations.

Customers & Market Segments

Smith & Nephew serves a broad spectrum of customers within the healthcare system, primarily healthcare providers:

Its direct customers are typically hospitals, surgical centers, and clinics that purchase its implants and devices. Within those institutions, the key decision-makers and users are surgeons and clinical specialists – e.g. orthopaedic surgeons for joint implants, sports medicine orthopedic surgeons for arthroscopy products, plastic surgeons or wound care nurses for wound management products, and ENT surgeons for the tonsil/adenoid devices.

It also interfaces with procurement departments and administrators who negotiate contracts (especially in large hospital networks or GPOs). Ensuring that its products demonstrate value (through improved outcomes or economic savings) is crucial to satisfy these stakeholders.

Given its diverse portfolio, Smith & Nephew effectively targets several market segments:

Orthopaedic Reconstruction segment: Customers here are orthopaedic surgeons and their patients needing joint replacements (often older adults with arthritis or younger patients with severe joint damage). These customers prioritize implant longevity, range of motion, and postoperative recovery time. Smith & Nephew addresses these needs with implants like the LEGION and JOURNEY knees and POLAR3 hips known for low revision rates, and by providing surgical tools (like navigation and robotics) that improve placement accuracy. The typical patient in this segment is in their 60s or 70s with osteoarthritis in a hip or knee, although younger active patients are also increasingly getting joint replacements. They “expect a fast recovery and rapid return to activity,” and surgeons want to operate as efficiently and minimally invasively as possible while ensuring the best outcomes.

Trauma & Extremities segment: Here the customers are trauma surgeons and orthopaedic specialists fixing fractures or extremity injuries. They need a wide range of implant sizes and types to address everything from simple wrist fractures to complex pelvic breaks. Smith & Nephew’s EVOS plates and TAYLOR SPATIAL FRAME external fixator cater to these needs. Key customer needs are stability of fixation, ease of use in emergency surgery, and availability of implants for varied anatomies.

Sports Medicine segment: The primary customers are sports medicine orthopedic surgeons and arthroscopic surgeons, often treating athletes or active individuals with ligament tears, shoulder injuries, etc. They value innovative repair techniques (like the REGENETEN patch for tendon repair) and comprehensive tool sets for arthroscopy (cameras, scopes, resection devices). A lot of these procedures occur in ambulatory centers, so this segment also values portability and efficiency. The patients are often younger (20s–50s) and highly motivated to recover quickly; thus, products that can potentially speed up rehab or reduce re-injury are very attractive. Smith & Nephew’s portfolio (from FAST-FIX meniscal repair devices to LUPO and ULTRABUTTON ACL fixation systems) speaks to these demands.

Ear, Nose & Throat (ENT) segment: Customers are ENT surgeons performing tonsillectomies, sinus surgeries, etc. They appreciate tools that reduce bleeding and pain – e.g. COBLATION◊ wands for tonsil removal which cause less tissue damage than traditional electrocautery. Patients (often children for tonsil cases) benefit from faster recovery and less pain.

Advanced Wound Care segment: The customers range from hospital wound care clinics to home healthcare providers. Wound care nurses and physicians use these products on patients with chronic wounds (diabetic foot ulcers, pressure ulcers) or postoperative incisions. Their priorities are accelerating wound healing, preventing infection, and reducing the frequency of dressing changes (which can be labor-intensive and costly). Smith & Nephew’s ALLEVYN◊ LIFE foam dressings, for instance, have features like an indicator for when to change the dressing and technology to lock in exudate, enabling longer wear time– this addresses the need to “do more with less” by requiring fewer dressing changes and freeing up nursing time. Another major need is preventing complications: a study showed using the PICO single-use NPWT on closed surgical incisions reduced the odds of infection by 63%, a huge benefit for patients and hospitals.

Customer profiles and satisfaction: Smith & Nephew’s customer base is global and diverse, but a unifying factor is that its end-users (surgeons, nurses) are highly trained professionals who demand reliability and proven outcomes. The company invests in close relationships – for example, it runs surgeon training programs (wet labs, virtual training, etc.) and partners on clinical research. In Italy, it even partnered with a hospital to enhance surgeons’ skills in hip surgery using its technologies. This engagement creates loyalty and ensures products are used to their full potential.

Feedback from the field often highlights that Smith & Nephew’s products “advance the standard of care” in their categories. Surgeons using the new AETOS shoulder system, for instance, can treat shoulder arthritis with both anatomic and reverse shoulder replacements using one platform, restoring patients’ range of motion and minimizing pain – early feedback on such innovations is positive. Hospital administrators appreciate when products can shorten hospital stays or reduce readmissions (e.g. fewer wound infections due to better dressings).

Another aspect of customer satisfaction is the company’s post-sale support and service. Smith & Nephew is known to have representatives in operating rooms to assist surgeons (especially for complex implant cases), and its “Ronin” remote assistance pilot with smart glasses (in partnership with Rods&Cones) allows reps to guide surgeries virtually. Such support improves the customer experience and confidence in using the products.

Geographically, the company adapts to customer needs as well. In the US (which accounts for ~50% of revenue), customers are very volume-driven and outcomes-focused – Smith & Nephew has tailored solutions like outpatient-friendly systems and value analysis support. In emerging markets (approx 19% of revenue), customers often seek a mix of advanced tech and affordability. The company launched, for example, its OR3O Dual Mobility hip system in India to bring a high-end implant to that growing market.

Customer needs summary: whether it’s an orthopaedic surgeon wanting a knee implant that bends more naturally, a sports surgeon needing a strong but absorbable implant for ACL repair, or a nurse needing a dressing that can stay on a wound for a week – Smith & Nephew’s strategy is to meet those needs through innovation. The ultimate customer is the patient, and they seek to reduce pain, restore function, and get back to normal life. By enabling its direct clinical customers to deliver those patient outcomes efficiently, Smith & Nephew creates value for all stakeholders.

Patient satisfaction is indirectly reflected in metrics like improved mobility scores or reduced re-operation rates using S+N products. Surgeons’ satisfaction is seen in repeat usage and inclusion of S+N devices in their standard practice. One notable point: each year ~14 million patients benefit from Smith & Nephew’s products , indicating the vast reach and acceptance in the marketplace. This breadth across multiple segments and geographies provides the company a balanced exposure to various customer segments, reducing reliance on any single therapy area.

Financial Performance

Smith & Nephew’s financial performance over the past few years shows a company that weathered the pandemic downturn and is now back on a growth trajectory, improving both its top-line and bottom-line metrics.

Smith+Nephew’s annual revenue fell sharply in 2020 due to pandemic impacts but has since rebounded to record levels by 2024

.

Revenue Trend: The company’s revenue was growing modestly pre-pandemic, hit a low in 2020, and has recovered strongly since. In 2019, Smith & Nephew had about $5.1 billion in revenue. Elective surgeries worldwide were postponed during the COVID-19 pandemic, causing 2020 revenue to drop to $4.56 billion (a steep decline of ~12%). However, in 2021, as surgeries resumed, revenue rebounded 14% on a reported basis to $5.21 billion, nearly back to 2019 levels. Growth then continued: 2022 was roughly flat (just over $5.2 billion) amid some supply chain and China headwinds, but 2023 saw a 6.8% underlying growth, bringing revenue to $5.5 billion. In 2024, Smith & Nephew achieved its highest ever revenue of $5.8 billion. In other words, from the 2020 trough, revenue has grown ~27%, reflecting a strong recovery. Importantly, growth in 2023–24 was driven by higher surgical volumes and new product introductions rather than pricing, as the company faced some pricing pressure (FX headwinds and China VBP). Underlying growth (which excludes currency swings) was around 5–6% in both 2023 and 2024, a clear step-up versus pre-2020 levels (when growth was ~4% . This indicates that Smith & Nephew’s 12-point plan to accelerate growth is bearing fruit with consistently higher revenue growth than in the past

.

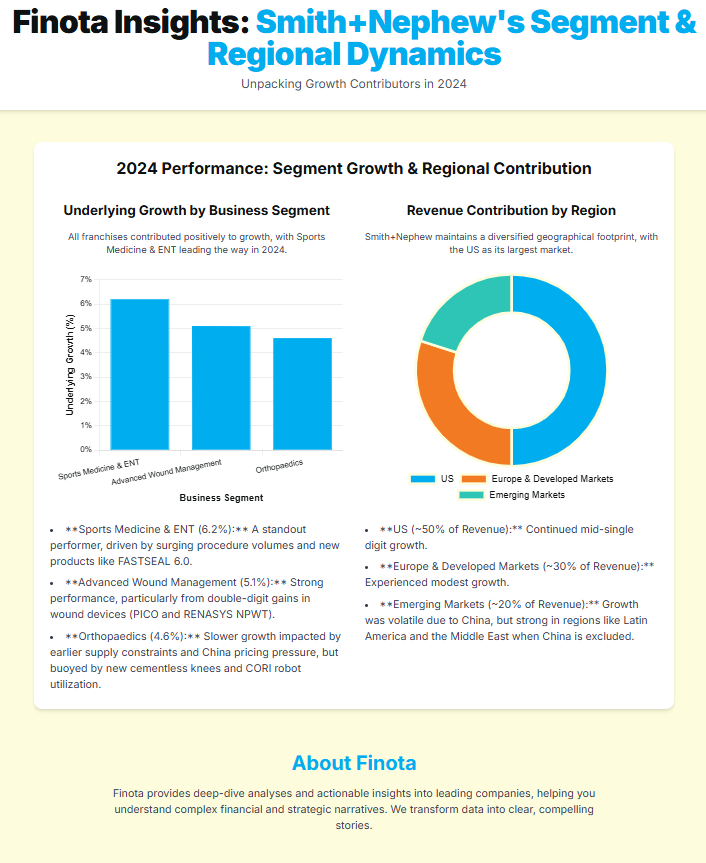

Segment and Regional Breakdown: The growth has not been uniform across segments, but encouragingly all franchises contributed. In 2024, Sports Medicine & ENT was a standout, with 6.2% underlying growth, as procedure volumes surged and new products like the FASTSEAL 6.0 hemostatic wand gained traction. Advanced Wound Management grew ~5.1% underlying, led by double-digit gains in wound devices (PICO and RENASYS NPWT sales were robust). Orthopaedics grew more slowly (about 4.6% underlying in 2024), reflecting supply constraints earlier and pricing pressure in China, but even there the knee implant sub-segment grew nicely (helped by new cementless knees and CORI robot utilization). Geographically, the US remains ~50% of revenue and grew in mid-single digits, Europe and developed markets are ~30% and grew modestly, while Emerging Markets (~20% of sales) are volatile due to China. Excluding China’s procurement cuts, emerging market growth was strong (Latin America, Middle East demand is rising)

.

Profitability: Smith & Nephew’s profitability has been improving, though it still lags some peers. The primary profit metric it reports is Trading Profit (an adjusted operating profit). For 2024, trading profit was $1.05 billion, which is an 18.1% trading profit margin. This marks an improvement from 17.5% in 2023 and 17.3% in 2022, indicating the company has turned the corner on margins. In fact, after a pandemic dip, margins are expanding again – partly due to cost-saving initiatives (the 12-point plan delivered over $200 million in cost savings, offsetting inflation) and partly due to operating leverage from higher sales. It’s worth noting that Smith & Nephew’s margin is lower than some competitors (who often post 25%+ in this industry), but the gap is closing. The orthopaedics franchise historically dragged on margin (in 2022 its margin was just ~18%, well below other franchises), but actions like simplifying the supply chain and closing excess facilities (four orthopaedic plants were closed by 2024) have started to lift it.

On a GAAP basis, the company’s net profit and EPS have grown significantly. In 2024, basic Earnings Per Share (EPS) was 47.2 cents, up 56% from 30.2¢ in 2023. This jump reflects higher operating profit and lower exceptional charges. Smith & Nephew also reports an adjusted EPS (EPSA) excluding one-offs – that was 84.3 cents in 2024, up slightly from 82.8¢. So, adjusted earnings are at record levels, though growing modestly as margin expansion is gradual. Importantly, these earnings now more fully cover the company’s annual dividend (~37.5¢ per share), which management held flat during restructuring and now plans to grow in line with earnings .

Cash Flow and Returns: One of the most striking financial turnarounds is in cash generation. Free cash flow (FCF) jumped to $551 million in 2024, from just $129 million in 2023. This huge improvement came from working capital efficiencies (inventory reduction after supply chain normalization) and lower restructuring payouts. The trading cash conversion in 2024 was excellent at roughly 95% of trading profit turning into operating cash. As a result, Smith & Nephew’s Return on Invested Capital (ROIC), a key measure of efficiency, has started rising. Adjusted ROIC increased by 150 basis points to 7.4% in 2024 (from 5.9% in 2023) , reflecting better profitability and asset utilization. While 7.4% is still below the company’s cost of capital (estimated ~8%), it’s moving in the right direction – management expects ROIC to exceed the cost of capital in 2025 for the first time in many years .

Comparative Performance: Versus industry peers, Smith & Nephew’s revenue growth in 2023–24 (~5–6% underlying) was on par or slightly above the medtech sector average. For instance, competitors like Stryker and Zimmer also saw mid-single-digit growth in their reconstructive businesses, while S+N’s sports/wound segments grew faster than many peers (benefiting from new products). In terms of margins, S+N is still below peer benchmarks, but the momentum is positive. Peers didn’t face as much margin erosion in 2020–22 as S+N did, so S+N’s current improvement has more catch-up potential. The company’s EPS growth (on an adjusted basis) has been modest (~2% CAGR over 2019–2024), but that masks the heavy investments and one-time costs. Now that those are largely behind, analysts expect EPS to accelerate in coming years, leveraging the higher sales.

Segment profit details: For insight, in 2024 the Sports Medicine & ENT franchise trading profit margin was 24.0% , Wound was ~23.7% (calculated from $399m profit on $1.68b sales ), and Orthopaedics was ~11.5% (after corporate cost allocation) . The blended 18.1% margin shows how improving Orthopaedics is key to lifting the overall margin. The company already improved Orthopaedics segment profit slightly in 2024 with better operations.

To sum up, Smith & Nephew’s financial health is on an upswing. It has emerged from the pandemic with record revenues, expanding margins, and vastly improved cash flows. The business mix – roughly 40% orthopaedics, 30% sports/ENT, 30% wound– provides multiple earnings streams, and all are growing. The focus now will be to continue that trajectory: management’s medium-term goal is to sustain ~5%+ organic growth and drive trading margin into the low 20% range. If it achieves this, EPS and ROIC should rise substantially, rewarding shareholders. The recent data suggests the company is indeed on track, with the 2024 results showing momentum in both growth and profitability. Investors will be watching that this momentum continues into 2025 and beyond, leveraging the large market opportunity in front of Smith & Nephew.

Financial Health

Smith & Nephew’s financial health is solid and has markedly improved in terms of leverage and liquidity in the last year. The company has a moderate debt load and ample liquidity, giving it flexibility to invest in growth while also returning cash to shareholders.

As of the end of 2024, Smith & Nephew had net debt of $2.51 billion (excluding lease liabilities) . This is a slight reduction from $2.58 billion a year prior, reflecting positive free cash flow used to pay down debt. Including lease obligations, net debt was $2.71 billion . The company’s balance sheet leverage is reasonable: on an adjusted basis, net debt is about 1.9 times EBITDA , down from ~2.1× a year ago . This leverage ratio of ~1.9× is comfortably within management’s target (they aim for ~2.0× net debt/EBITDA to maintain an investment-grade profile) . It’s also moderate compared to peers in the medtech sector, many of whom carry between 1–3× EBITDA in debt. The company’s interest coverage is healthy as well – in 2024, net interest expense was $121 million against an operating profit of $837 million (IFRS basis), meaning EBIT/interest coverage well over 6×. Even on a cash flow basis, interest was easily covered by operating cash flows. While rising interest rates did increase Smith & Nephew’s interest expense in 2023–24 (interest expense rose from $80 m in 2022 to $145 m in 2024) , the company has a good mix of fixed-rate debt and manageable maturities that mitigate risk.

Smith & Nephew maintains strong liquidity reserves. It has access to about $4.1 billion in committed credit facilities, with an average maturity of 5.5 years . At year-end 2024, it had substantial undrawn credit lines and a cash balance (cash and equivalents) of around $0.5 billion, which together provide more than enough liquidity for operational needs and any short-term debt repayments. The company’s debt maturities are staggered (including a mix of US private placement notes and bank loans) and it faces no liquidity crunch. Management has emphasized a balanced capital allocation: first investing in innovation and growth, then maintaining its investment-grade credit rating, and finally returning any surplus to shareholders (e.g. via dividends or potential buybacks).

Solvency ratios are comfortable: the net debt to equity ratio is moderate (equity is ~$4.6 billion, so net debt/equity ~55%). The company’s interest coverage and fixed charge coverage well exceed bond covenants. Indeed, Smith & Nephew was in full compliance with all debt covenants in 2024 with significant headroom . Rating agencies regard the company as investment grade (Moody’s and S&P have stable outlooks) given the consistent cash flows from the medical device business and the relatively low cyclicality of healthcare demand.

A highlight of 2024 was the surge in free cash flow to $551 million . This was driven by improved profitability and disciplined working capital management – inventories were brought down and receivables collected faster as supply chain issues eased. Free cash flow conversion (FCF as a percentage of net income) was over 100%, indicating high earnings quality. Such cash generation allowed Smith & Nephew not only to reduce debt but also to cover its dividend payments (which totaled around $330 million annually). The dividend has been held steady at ~$0.375 per share (roughly $330m) in recent years, and from 2025 onward the company plans a progressive dividend targeting a 35–40% payout of earnings. Given 2024’s EPSA of $0.843, the payout ratio was ~45%, slightly above target, but with earnings set to grow, the dividend is well-supported. The company even hints at the possibility of share buybacks if surplus cash accumulates and leverage stays at or below target.

Working capital and liquidity management improved significantly under the 12-point plan. Inventory days which had spiked during the pandemic (due to safety stocks and supply disruptions) started to normalize, freeing up cash. The company also reported a 90% reduction in overdue orders by 2024 compared to 2022, meaning supply chain issues have largely been resolved and are no longer tying up capital in backorders .

From a solvency risk perspective, Smith & Nephew’s business has low default risk: it enjoys steady demand, strong margins, and now robust cash flow. The biggest potential uses of cash (besides the dividend) could be acquisitions – management has stated interest in bolt-on acquisitions in high-growth segments . But with the current balance sheet, it has room to spend perhaps $1–2 billion on acquisitions without stretching leverage beyond 3× EBITDA. And thanks to the cash flow uptick, even such spending could be partially financed internally.

To ensure resilience, the company also addresses financial risks: it hedges currency exposures (since it reports in USD but has significant GBP and EUR costs, as well as emerging market currencies to consider). It also monitors pension obligations, but note that its UK pension fund is closed and mostly derisked (and in slight surplus), so not a big cash drain.

Smith & Nephew’s financial health is strong and getting stronger:

Leverage: moderate and on a downward trend (Net Debt/EBITDA ~1.9× , well within comfortable range).

Liquidity: abundant with large credit lines and improving cash generation.

Coverage: interest obligations are well-covered by earnings (interest cover >6–7×).

Cash flow: turning into a significant strength – FCF of $551m in 2024 is 10% of sales, a great sign of financial efficiency . This cash can fund growth investments, debt reduction, and shareholder returns simultaneously.

Financial discipline: The company has pledged to maintain an optimal balance sheet and investment-grade credit metrics , and 2024’s results show delivery on that promise.

Barring a major unforeseen downturn, Smith & Nephew is financially equipped to pursue its strategic objectives without needing to raise equity or excessive debt. Its financial health should also provide stakeholders (customers and suppliers) confidence in the company’s stability. In a field like medical devices, a strong balance sheet is a competitive advantage because it allows consistent R&D investment and service levels even during economic hiccups. Smith & Nephew appears to have achieved that stability now.

Strategic Position

Smith & Nephew’s strategic position can be analyzed by looking at its internal strengths/weaknesses and external opportunities/threats (SWOT), as well as through the lens of Porter’s Five Forces in its industry. We can also consider recent strategic moves like acquisitions and partnerships that shape its positioning.

Strengths: Smith & Nephew has several key strengths:

Broad and Diversified Portfolio: The company is active in three major medtech domains (orthopaedics, sports/ENT, wound) which gives it multiple revenue streams and reduces dependence on any single product. These franchises collectively cover a wide range of healthcare needs – from elective joint surgeries to acute trauma and chronic wound care – providing some hedge against market fluctuations. Notably, its faster-growing franchises (Sports Medicine & Wound) make up about 60% of sales, balancing the slower orthopaedics segment .

Innovation and R&D Capability: Smith & Nephew has a strong track record of product innovation, which is crucial in medtech. Over the past few years, it has introduced wave after wave of new products – more than 60% of its 2024 revenue growth came from products launched in the last 5 years . Examples include the REGENETEN implant, the CORI robotic system, new materials like CONCELOC◊ 3D-printed porous titanium for implants, and PICO NPWT in wound care. This pipeline of innovation fuels growth (roughly 3.5 percentage points of its annual growth in 2023–24 came directly from new products ). By continuously updating its portfolio, S+N stays relevant and often has best-in-class offerings (e.g. clinical data showing its products significantly reduce complications).

Global Market Presence and Brand: With sales in over 100 countries and a particularly strong presence in Europe and emerging markets (in some emerging regions S+N outranks larger US rivals), the company has built deep relationships with surgeons worldwide. It is often the #2 player in markets outside the US in its categories, benefiting from legacy and local strategies. The brand name “Smith & Nephew” is associated with quality (some hospitals specifically request its wound dressings or its BHR hip resurfacing system, for example). Being in the FTSE100 and a consistent operator gives it a solid corporate reputation.

Focused Strategy and Execution Improvement: Since 2022, the new leadership’s 12-point transformation plan has fixed many structural issues and streamlined operations. The company improved supply chain reliability (huge reductions in backorders) and undertook cost efficiencies like facility rationalization . Now with much of the heavy lifting done, S+N is a leaner organization poised to reap operational leverage. The cultural focus on “efficient execution” is paying off in margin uptick and better alignment of the business units. As the Chairman noted, they are embedding a more accountable, performance-driven culture while reinforcing leadership positions . This internal strength in execution bodes well for hitting strategic goals.

After-sales Service and Customer Support: S+N’s support network (field reps, training programs) is seen as a strength, fostering loyalty among surgeons. This is somewhat intangible but a crucial differentiator especially in orthopaedics where close surgeon relationships matter.

Weaknesses: Some areas that Smith & Nephew needs to improve or which have been historical drawbacks include:

Lower Profit Margins vs Peers: While margins are improving, the company’s trading profit margin (~18% ) is still below competitors like Stryker or J&J, which often have 25–30% margins in medical devices. Part of this is due to the orthopaedics segment – it has lagged with ~11–18% margins historically, dragged by higher costs and prior inefficiencies . This means S+N has had less room on price or to invest compared to rivals. It’s addressing this through supply chain fixes and cost cuts, but it remains a relative weakness in financial efficiency.

Orthopaedics Segment Challenges: Within its portfolio, orthopaedics (hips/knees and trauma) has underperformed. Its global market share in hips/knees is ~10% , significantly behind the top 3 players. It lost some share in the past in the US market due to supply issues and perhaps a slower adoption of robotics early on. Additionally, China’s VBP hit this segment’s growth hard (hip and knee sales in China dropped due to price cuts). Trauma, where it has only ~4% global share , has been a weak spot – S+N is a smaller player in trauma and has fewer products than big rivals. Being sub-scale in trauma might limit its ability to compete for large hospital deals that bundle trauma with other implants. Overall, orthopaedics franchise profitability and share are a weakness (but also an opportunity if turned around).

Exposure to External Shocks: As seen during the pandemic, Smith & Nephew’s sales dipped more sharply than some diversified peers (like J&J, which has pharma division to buffer device declines). While it’s diversified within devices, it doesn’t have other health sectors to cushion a complete elective surgery shutdown. This is a general medtech weakness but notable. Also, being UK-headquartered, it reports in USD but incurs costs in various currencies, causing FX volatility (in 2022, for instance, a strong dollar created a 5% revenue headwind – that’s somewhat out of management’s control).

Historically Slow-to-Market in Some Tech: In certain instances, S+N has lagged competitors – e.g. in large-joint robotics, Stryker’s Mako robot was out years before CORI. In spine surgery and cardiothoracic (areas adjacent to ortho), S+N has no presence, whereas some competitors diversified there. This isn’t core to S+N’s current focus, but it means they don’t participate in some growth sub-sectors (spine, dental implants, for example). They have sometimes been perceived as followers rather than first-movers in innovation (though REGENETEN and others show that’s changing).

Geographical Overlap Weakness: The US is 50+% of sales, which is typical, but S+N’s US ortho market share is lower than its global average. It’s sometimes struggled with the large hospital systems in the US that prefer full-line suppliers; S+N’s narrower trauma offering hurt it in those tenders. The company has acknowledged past commercial execution issues in the US recon market and has been working to improve its salesforce effectiveness . Until recently, that was a weakness – now improving but still regaining lost ground.

High Cost Base: Being a company that historically manufactured in high-cost locations (US, UK, Europe) with some inefficiencies, S+N’s gross margins were a bit below peers. They are addressing with new plants (e.g. in Malaysia, Costa Rica) and outsourcing. But it’s a slow fix; in the interim, inflation in 2021–2022 hit margins more since it had a higher cost baseline.

Opportunities: Smith & Nephew has multiple growth opportunities externally:

Market Growth and Aging Demographics: The macro trend of aging populations is a rising tide – by 2030, 1 in 6 people globally will be over 60. This means more knee and hip replacements (often people want to stay active longer) and more chronic wounds (due to diabetes, etc.). Smith & Nephew’s core markets are projected to grow ~4–6% annually in coming years just from these demographic tailwinds . The company can capitalize on this by ensuring it captures more than its share of new patients. For instance, joint replacements in emerging markets (China, India) are far below Western rates – as healthcare access improves, huge volumes of new surgeries could come. Smith & Nephew has an opportunity to be a provider of choice in those emerging markets by offering a range of products at different price points.

Geographic Expansion & Emerging Markets: While China has been challenging (due to pricing reform), other emerging markets are booming. Smith & Nephew is expanding in India, Latin America, Middle East, and Africa where growth rates are high. It launched tailored products like the OR3O dual mobility hip in India in 2023 and is expanding its distribution network. Also, once China’s pricing stabilizes, volumes there could still benefit S+N (China did ~10% of S+N’s business pre-VBP, and even at lower prices, unit growth means more procedures done). If S+N can manage costs, emerging markets present a long-term growth runway with millions of untreated patients.

Product and Technology Innovation: This is an internal strength, but also an opportunity to drive future growth. S+N has a rich R&D pipeline. For example, it acquired CartiHeal in 2024 – this gives it the Agili-C implant for knee cartilage regeneration , addressing a huge unmet need for early knee arthritis treatment. If Agili-C can delay knee replacements by repairing cartilage, it opens a new market for S+N (younger patients). Similarly, new robotics features (they are adding augmented reality and smart mapping to CORI) and AI-driven surgical planning tools (like RI.INSIGHTS™ which uses AI to guide knee implant alignment ) can differentiate S+N’s offering and attract tech-savvy surgeons. The INTELLIO◊ platform connecting all arthroscopy devices and new sports medicine implants (like the UltraTRAC◊ ACL system) also give opportunities to upsell to existing customers.

Portfolio Expansion via M&A: Smith & Nephew has shown it will use acquisitions to fill gaps – e.g. buying Osiris for regenerative skin products, Integra’s extremities business to get into shoulder replacements, and now CartiHeal. It explicitly states part of its strategy is to “invest in acquisitions targeting new technologies in high-growth segments” . The opportunity here is that S+N could acquire a company in, say, robotic-assisted trauma surgery or a digital health platform for wound care, enhancing its future growth. With its relatively lower valuation than some peers and strong cash flow, S+N might also be able to do accretive deals that competitors find too small or niche.

Improving Orthopaedics Market Share: There is a lot of low-hanging fruit if S+N can regain share in orthopaedics. For example, in knee replacements, introducing the new cementless knee and CORI robot could let it recapture hospital accounts it lost. The US orthopaedics market is an opportunity: even a few points of share gain (from 10% to 12–15%) in the $16B hip/knee space would significantly boost revenue . Ambulatory Surgery Centers (ASCs) are a specific growth area in the US where S+N is well-positioned (they offer tailored ASC packages) – as more joint surgeries move to ASCs, S+N can capture those if it markets effectively to outpatient-oriented surgeons .

Healthcare System Trends to Value: There is an opportunity as payers move to value-based care – S+N’s products that demonstrably reduce complications or length of stay can shine. For instance, data that PICO dressings cut infection rates, or that their knee implants lead to faster rehab, can be used to negotiate better access or even share in cost savings. If S+N can package solutions (device + support + data) to help hospitals improve outcomes, it becomes a partner rather than just a vendor, potentially capturing more business.

Threats: The company does face external threats and risks:

Intense Competition and Pricing Pressure: As discussed, larger competitors with broad portfolios can bundle deals (e.g. offering discounts on hips if a hospital also buys their knees and trauma). Smith & Nephew must contend with that by offering competitive pricing or superior tech. There’s a threat that if it cannot match the depth of a competitor’s offering (especially in trauma or spine which S+N doesn’t have), some customers might choose a one-stop competitor. Moreover, pricing pressure is a persistent threat – not only VBP in China, but in the US insurers push back on high costs, and in Europe tenders often go to lowest bidder if products are seen as commodities. We already saw this with China’s VBP causing a significant price and volume loss in 2022–24 . If such models spread (e.g. possible expansion of tenders to sports medicine implants or NPWT devices by large hospital chains), it could erode margins and market share.

Regulatory and Compliance Risks: The medtech industry is heavily regulated. A recall of a major product (due to safety issue) could be very damaging. For example, if evidence emerged of a problem with a widely used implant, S+N could face lawsuits and loss of trust (consider what happened with metal-on-metal hips historically – not S+N’s, but generally). There’s also the new EU Medical Device Regulation (MDR) which imposes stricter requirements – S+N must ensure all its legacy products get recertified or it could lose the ability to sell them in the EU. They budget for MDR compliance (noting costs in guidance ), but it’s a heavy effort. Additionally, regulatory approvals for new products can be slower or costlier than anticipated, which might threaten pipeline timelines.

Supply Chain and Operational Disruptions: As a manufacturer, S+N is exposed to potential supply disruptions – whether it’s a shortage of a key raw material (like titanium or semiconductor chips used in capital equipment) or disasters affecting its major plants. Its production is concentrated in a number of key facilities (Memphis, Hull, etc.) ; a fire, flood, or geopolitical issue could halt production. In 2022, for example, semiconductor shortages held back some sales in the arthroscopic enabling tech segment – a reminder that even a medtech can be hit by global supply issues. The company does mitigate with multiple sourcing, but threats remain (including cyber-attacks on factories or logistics).

Macro-economic and Currency Threats: Strengthening of the US dollar can reduce reported revenue and profit (as happened in 2022 when revenue growth was cut by ~5% due to FX ). High inflation in manufacturing costs could also pressure margins if S+N cannot raise prices equivalently (healthcare budgets are tight, so passing on inflation is not always possible). Recessionary environments could lead governments to cut healthcare spending or delay capital purchases by hospitals, indirectly threatening S+N’s sales (though elective surgeries tend to be more need-driven than economic-driven).

Lawsuits and Product Liability: This is a standard threat in medical devices – if any product results in patient harm or is alleged to (even incorrectly), it can result in costly litigation or settlements. For instance, wound care products or surgical tools used improperly could be subject to claims. S+N must maintain rigorous quality control and monitoring to mitigate this.

Competitive Innovation: The flip side of S+N’s innovation opportunity is the threat of competitor innovation. If a competitor launches a truly breakthrough technology – say, a new biomaterial or a revolutionary robotic system – it could make some of S+N’s offerings less attractive. For example, if a rival sports medicine company created a biologic that heals ACL tears without surgery, it would disrupt the surgical devices market S+N plays in. Thus, S+N must keep pace, or risk being out-innovated. The medtech field is full of emerging tech: AI diagnostics, 3D-printed implants, gene therapies, etc. Not all directly compete with S+N, but some could in the future.

Porter’s Five Forces Analysis:

Competitive Rivalry – High: Few large rivals and many smaller players create a fiercely competitive environment. Pricing battles (especially in tenders) and feature-for-feature product competition are routine. Smith & Nephew must continuously differentiate to avoid commodity status.

Threat of New Entrants – Low to Moderate: While new entrants face high barriers (regulatory, need for clinical evidence, sales network), the lure of high margins means startups do pop up (especially in niche areas like biotech wound care or specific sports injuries). However, most need to partner with or be acquired by firms like S+N to reach scale. Large tech firms entering medtech is a theoretical threat but less likely in S+N’s spaces (Google won’t suddenly make wound dressings, for instance).

Threat of Substitutes – Moderate: The substitute for a surgical device is often a non-surgical therapy. For example, could physical therapy or injections delay a knee replacement? Yes, sometimes. Or could improved preventive care reduce chronic wounds? Possibly. There’s also the substitute of doing nothing (patients enduring disability). However, given the efficacy of these surgeries and therapies, substitutes often are inferior. Still, any breakthrough in pharmaceuticals (like a drug that regrows cartilage or heals wounds ultra-fast) could substitute for using devices. So S+N keeps an eye on adjacent fields (they acquired a biotech-like product Grafix to not be left out of biologics for wounds).

Bargaining Power of Suppliers – Low: S+N’s suppliers are generally commodity materials (metals, polymers, electronics) where S+N is a big client, so not much power for suppliers. One exception is if a particular patented biomaterial or component is sourced – but S+N often has dual sources or makes in-house. The biggest “supplier” might be highly skilled labor or surgeon design inputs – not traditional supplier, so not a major threat.

Bargaining Power of Buyers – High (increasing): Buyers (hospitals, health systems) have consolidated. They use tenders and bulk contracts to demand discounts. Governments (especially single-payer systems) also exert strong pricing power (e.g. UK NHS or German insurers negotiating hard). In China, the buyer is literally the state doing group procurement – extreme buyer power. The trend of hospital consolidation and centralized purchasing raises buyer power, pressing margins. To mitigate, S+N tries to offer unique value (data, training, outcomes) to be seen as a partner not just a supplier.

Recent Strategic Moves (M&A, Partnerships, Divestitures):

Smith & Nephew has been actively shaping its portfolio:

In 2024, it completed the acquisition of CartiHeal for an upfront ~$70m (and potential milestones of several hundred million) . Strategically, this brings a breakthrough cartilage regeneration implant (Agili-C) which could create a new category of sports medicine treatment for early osteoarthritis. This not only opens revenue opportunities but also complements S+N’s knee implant business (patients could get Agili-C earlier in life, and perhaps S+N knee later – capturing the full patient journey). It’s a great example of using M&A to seize technology.

In 2021, it acquired the Extremity Orthopaedics unit of Integra LifeSciences, which gave it a direct presence in shoulder replacements and a dedicated extremities sales channel. This filled a gap – shoulders are a fast-growing segment and S+N now has a state-of-the-art AETOS◊ shoulder system launched in 2023 to compete there . This acquisition is already bearing fruit as AETOS enters the market and S+N leverages the specialized salesforce.

It also acquired Osiris Therapeutics in 2019 (for skin substitutes like Grafix) and Leaf Healthcare (for a wireless patient monitoring system for pressure injuries) in 2019. These moves boosted its Advanced Wound Bioactives and digital portfolio, aligning with the trend of biologics and digital in wound care.

On the divestiture side, Smith & Nephew hasn’t done major sell-offs recently (having earlier divested its gynaecology business in 2016 and therapy brands in prior decades). It appears focused on core segments now. It did divest a distribution joint venture in 2022 and some minor assets, but nothing transformative.

In terms of partnerships, one notable one is with Rods&Cones (a remote surgery visualization firm) to provide smart surgery glasses, allowing S+N reps to virtually “see” from the surgeon’s perspective in the OR . This digital partnership is innovative in customer support. Another partnership: S+N is part of the HGP consortium working on antimicrobial resistance in wounds. And in sports medicine, they sometimes partner with academic institutions for clinical trials or with startup incubators to get early looks at tech.

The company has also been investing in robotics partnerships – e.g. working with Brainlab for some navigation tech integration in the past, and likely exploring more tie-ups in surgical AI and data (though specifics are under wraps).

All these moves indicate a strategy to “Strengthen, Accelerate, and Transform” (as S+N puts it) – strengthen core via efficiencies, accelerate growth via innovation and M&A, and transform through new business models and digital technologies.

Overall Strategic Position: Smith & Nephew stands in a solid but challenging position – it is a top-tier medtech player with leading positions in select niches (like sports medicine and wound care), but also an underdog in others (like orthopaedics) where it must fight to gain ground. It is leveraging its strengths in innovation and wide portfolio to capture opportunities like growing emerging markets and new surgical techniques. At the same time, it remains exposed to industry threats of price pressure and fierce competition, which it is mitigating through differentiation and efficiency drives.

The company’s recent strategic actions (cost restructuring, targeted acquisitions) have shored up internal weaknesses and positioned it to be more agile and focused. A quick SWOT recap:

S (Strengths): broad portfolio, innovation, global reach, improving execution.

W (Weaknesses): sub-peer margins, ortho market share gap, reliance on surgical volumes.

O (Opportunities): aging demographics fueling demand, emerging markets expansion, new tech (robotics, biologics, AI) to lead in, orthopaedics turnaround, tuck-in acquisitions.

T (Threats): competitor actions, pricing cuts, regulatory hurdles, macroeconomic factors, substitute therapies.

Smith & Nephew’s strategic position is thus one of a company in transformation – leveraging its heritage and broad base to seize new growth, while actively addressing past shortcomings. If it continues executing well, it can strengthen its foothold in the medtech competitive landscape and perhaps even leapfrog in certain areas (for instance, by dominating the outpatient surgery segment or regenerative sports medicine space). Its focus on Life Unlimited ensures its strategy remains tethered to improving patient outcomes, which is both noble and smart business in an era of value-based care.

Future Potential

Looking ahead, Smith & Nephew’s future potential appears bright, underpinned by favorable market dynamics, new technologies, and strategic plans that could significantly enhance its market position. The company has articulated a clear vision for growth and is making investments to realize it. Here are some key aspects of its future potential:

Market Share Expansion: There is considerable room for Smith & Nephew to increase its market share in several segments. In orthopaedics, as noted, it holds about 10% of the global hip and knee implant market , versus the leader’s 30%+. Capturing even a few additional percentage points would translate to hundreds of millions in revenue. The company’s strategy to do this revolves around its new products and improved commercial execution. For example, the LEGION CONCELOC◊ cementless knee and the CATALYST◊ primary hip system (launched in 2024) are designed to meet modern surgical preferences (cementless implants, suitable for outpatient surgery, etc.) . Early surgeon feedback on these has been positive, citing improved precision and ease. Additionally, the CORI surgical robot, now with 1,000+ units installed globally, is a growth engine – each robot placement tends to lock in a hospital to S+N implants and can drive procedure volume growth (S+N noted that about one-third of knee procedures in the US are done robotically now , so having a competitive robot is crucial). As CORI continues to roll out (especially in markets where rivals haven’t penetrated as much, like Latin America or Middle East), S+N can win share.

In Sports Medicine, Smith & Nephew already is a leader, but it can consolidate or even grow that lead by expanding into new procedures. The acquisition of CartiHeal’s Agili-C implant for cartilage repair is a case in point – it opens the door to treating early knee osteoarthritis patients, potentially a large new market adjacent to sports injuries. If S+N can be first to effectively commercialize a cartilage regeneration solution, it could dominate a space with few alternatives, adding to its ~28% sports medicine share . Also, as shoulder repair and ankle repair techniques advance, S+N’s comprehensive sports medicine plus extremities portfolio can capture more of those cases (with AETOS shoulder and the new foot/ankle plating systems launched in 2024). There’s an opportunity to cross-sell: a sports medicine surgeon who already uses S+N scopes and shavers might adopt S+N’s shoulder replacement for their arthroplasty cases, since the company now offers that too.

Growth Drivers: A major driver of future growth will be innovation adoption. Smith & Nephew expects around 3–4 percentage points of its annual growth to come from new products (they achieved ~3.5 points from innovation in 2023 and 2024) . Some exciting specific drivers:

Robotics and Digital Surgery: The continued uptake of the CORI robot (which uniquely can be used for partial, total, and revision knees on one platform ) will drive implant sales. Moreover, S+N is enhancing CORI with new digital capabilities – e.g. the upcoming CORIOGRAPH◊ pre-operative planner and RI.HIP◊ Navigation allow surgeons to plan cases with AI and perform hip replacements with navigation on CORI . This should make the system more attractive and sticky. The company noted it has launched 10 new CORI features since 2022 and has more coming (like video-based mixed reality navigation) . This wave of improvements could lead to surgeons preferring Smith & Nephew’s digital surgery ecosystem, boosting growth.

Ambulatory Surgery Centers (ASCs): As mentioned, procedures moving to outpatient centers is a growth vector. Smith & Nephew is tailoring product bundles specifically for ASCs (e.g. efficient instrument trays like the CATALYST hip’s single-tray system for easy setup ). It claims to be uniquely positioned for ASCs by offering implants plus sports plus wound care for post-op – a full continuum . The ASC trend could accelerate, especially in the US, and S+N could gain share if its salesforce targets these centers effectively.

Emerging Market Growth: Over the next decade, markets like India, China (even with VBP, sheer volume growth will be large), Southeast Asia, and Africa will likely contribute a growing portion of medtech demand. Smith & Nephew, with its historical emerging markets presence (in Latin America, it’s strong; in China, still #4 in ortho even after VBP), stands to benefit. If China’s implant volumes double (as more patients get access) even at lower prices, S+N could still see good revenue. And in places like India, they are launching value variants of products to capture mid-tier segments. Market share in emerging regions is often up for grabs since not all competitors have direct operations there – S+N can build loyalty early.

New Adjacent Markets: Smith & Nephew might expand into some adjacent categories in the future – for instance, it has no spine surgery products currently, but that’s a large ortho adjacency. There have been speculations it could partner or acquire to get into spine or digital physical therapy monitoring, etc. While not confirmed, tapping into any new segment would be upside potential.

Technology and Innovation Pipeline: The future will also see continuous product upgrades:

In orthopaedics, smart implants (with sensors that transmit data on performance) are an emerging concept. S+N has invested in R&D for sensor-enabled knee implants that could monitor range of motion or load. If such technology matures, S+N could be at the forefront and differentiate in a big way.

In wound care, the pipeline includes next-generation dressings (even more absorption, antimicrobial properties) and likely more digital solutions like the LEAF◊ patient monitoring for pressure injury prevention . The combination of devices with data analytics (imagine wound dressings that track the wound healing progress via connected apps) might become reality and S+N is trialing such concepts.

Biologics: S+N could bring to market new biologic therapies – perhaps further placental tissue products or growth factor gels – which complement its devices. This could create new revenue streams and make their offering more holistic (device + biologic together for improved healing).

Geopolitical and Expansion Plans: Smith & Nephew has also indicated plans to expand manufacturing in cost-effective regions (for instance, a new plant in Malaysia came online for orthopaedic instruments, and Costa Rica for sports medicine). By 2025 and beyond, these moves will lower production costs, aiding margins and allowing competitive pricing, which indirectly fuels potential market share gains in price-sensitive markets.

Market share evolution: We could realistically see Smith & Nephew going from ~7–8% global medtech share (within its served markets) to maybe 10%+ in the next decade if it executes well, given many rivals are larger but more entrenched in slower-growth areas (like J&J’s DePuy is big but J&J is focusing more on pharma now, potentially giving S+N room to shine in medtech focus).